When I was 22, I graduated from college with $85,509 in debt 👀

Fast forward 7 years, and my net worth just crossed the $500k range - before the age of 30.

This wasn't because of some secret hack.

I followed a handful of slightly uncomfortable strategies that I picked up from some of the best personal finance and business books 📚

So today, I want to break down the exact framework that I used to go from $85k in debt to a half a million net worth.

💼 Increasing Your Income (Years 1–2)

This one sounds obvious… and also kind of annoying as a "strategy."

But the reality is you cannot budget your way to wealth when you simply aren’t making enough.

When I was 23, I was making $72k a year.

After rent, loans, and basic living expenses, the absolute most I could save was about $150/month.

One flat tire.

One sick day.

One broken phone.

And months of “progress” disappeared.

📉 Spending less was not the problem

📈 My income was

So I focused on aggressively increasing it:

- I went all‑in on my 9-5: reading books, taking courses, even learning to code so I could build automations and work faster - all in an effort to get promoted

- If I didn't get promoted within 2 years, I switched companies and gave myself my own "promotion"

- When I was 24, I even started my own small business - generating even more income

I share my entire engineering salaries throughout my career in the video linked at the bottom of this newsletter - if you are curious 👀

🤵🏼 Managing Lifestyle Creep (Year 3)

Once your income reaches a point where saving is finally realistic, the challenge changes.

Income isn't your problem any more, lifestyle creep is.

It’s incredibly easy to accidentally spend more as you increase your income:

- Upgrading your apartment

- Travelling to new places

- Eating out all the time

…and you might realize you are saving the same $150/month as before when you made significantly less 😬

But you don’t have to cut everything, what I did was adopt conscious spending.

Things I don’t spend much on:

- 🏠 Housing

- ✈️ Travel

- 🎟️ Concerts & entertainment

- 👜 Luxury goods

- 💄 Beauty services

Things I never limit:

- 📚 Books

- 🎓 Courses & education

- 📑 My hobby (scrapbooking)

- 📦 Time‑saving services & software

The goal is to be a bit more intentional with your spending.

🧠 A Quick Note on Time vs Money

One mistake I see a lot:

People save money… by spending huge amounts of their time.

🍳 Cooking everything from scratch

✍🏼 Doing tasks that could easily be automated

That’s why I don’t cheap out on tools that save me time.

And one of my favorite tools is Scribe.

They have a tool that automatically turns workflows into step‑by‑step guides - saving me from endless explanations, screenshots, and calls.

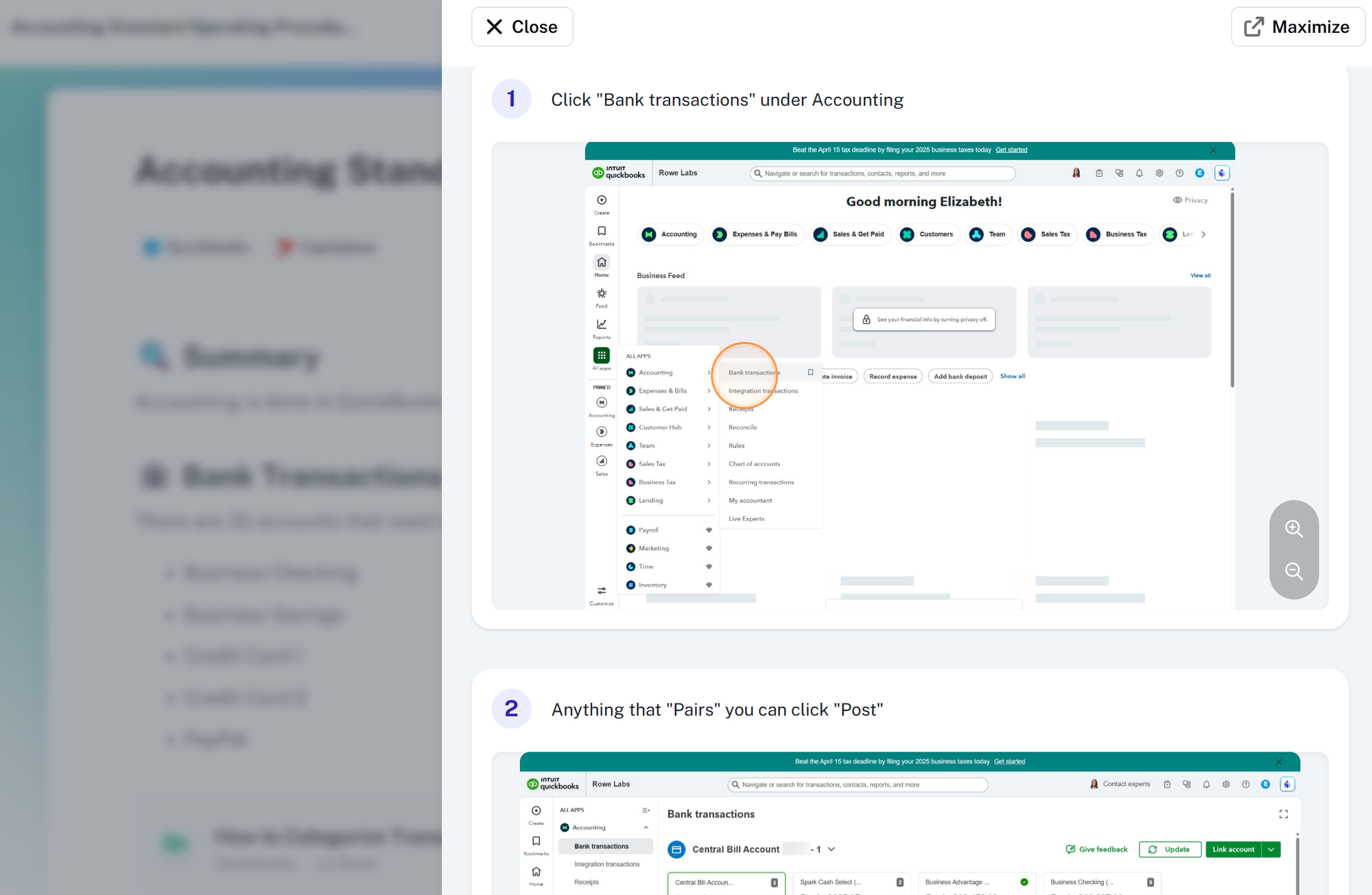

I especially love using Scribe to document standard operating procedures (SOPs) for my business like an accounting SOP that I can hand to an assistant while I go on vacation:

👉🏼 If you want to check them out, you can try their free plan here.

📃 Tracking Your Cash Flow (Year 4)

This is where things really started to compound.

I do what I call a “cash audit” every 15 days.

The goal is simple:

- 💰 Know how much you’re saving

- 📈 Know your total net worth

... every single month

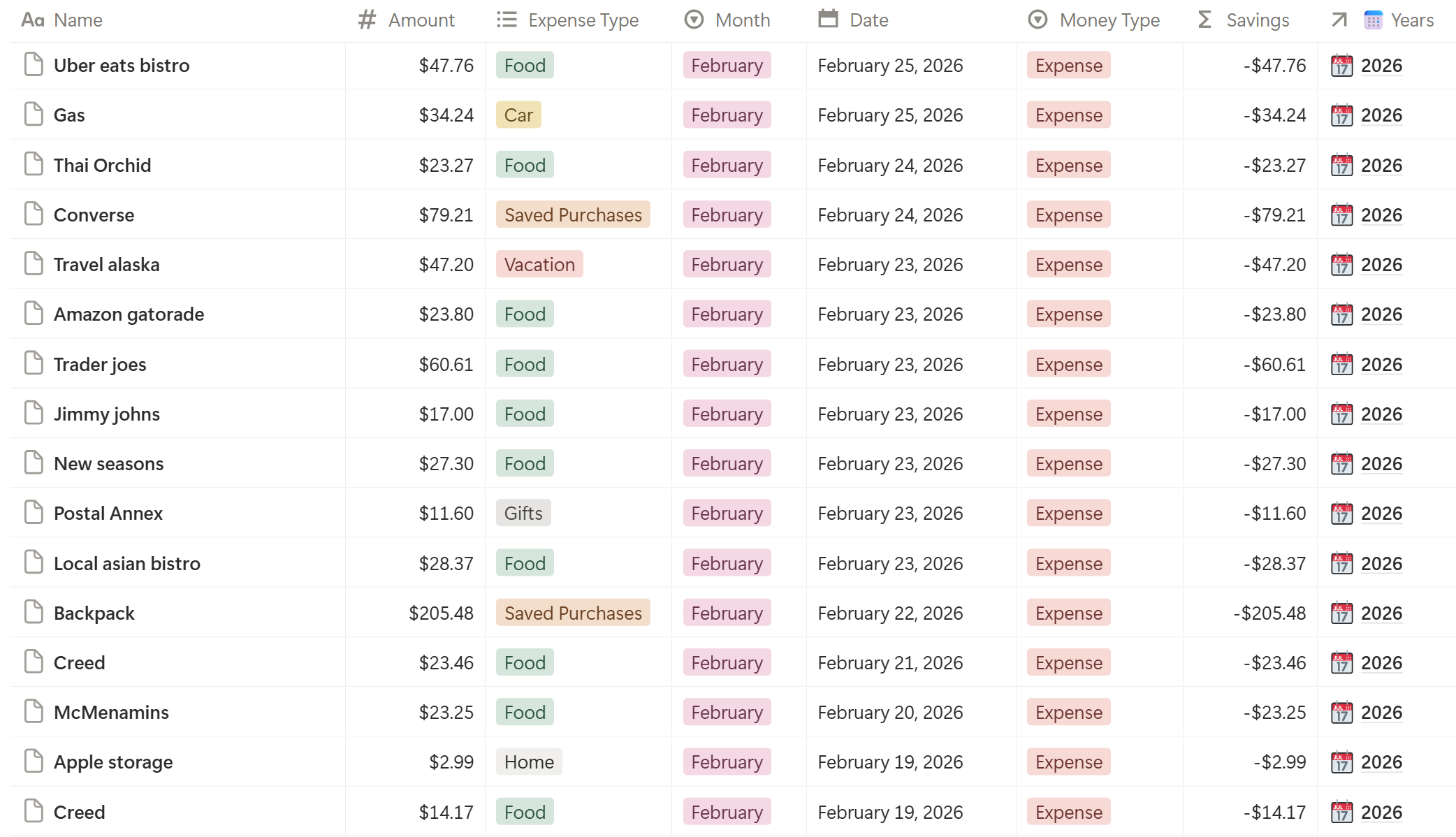

To know how much I am saving, I manually track every transaction in Notion (but Excel works too).

Yes - it’s a little tedius!

Typing in a $75 Uber Eats charge into your little Excel spreadsheet hurts in a way a budgeting app never will 👀

I use a separate database in Notion (or use Excel) to track net worth. This is incredibly motivating (unlike the expense tracker!).

Shoutout to my friend Pat for showing me how he built his in Excel (I copied his idea, but of course use Notion instead 😇).

I have a whole video on how I built my net worth tracker here.

🪙 Short‑Term Savings (Years 5–6)

Once I knew exactly how much I was saving, I needed to protect my money from myself (lol).

That meant:

- Moving money out of my checking account into high‑yield savings accounts for short‑term goals

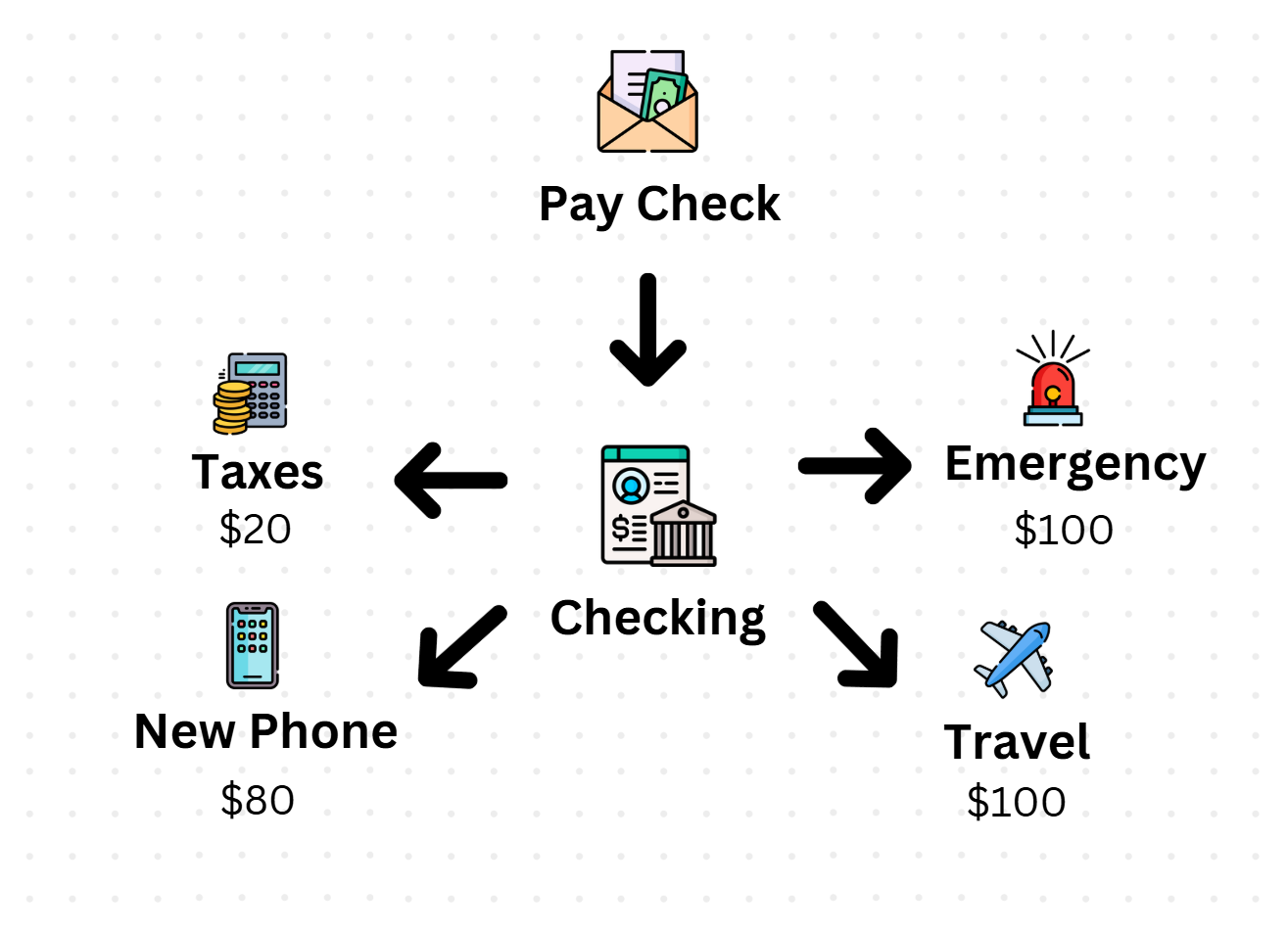

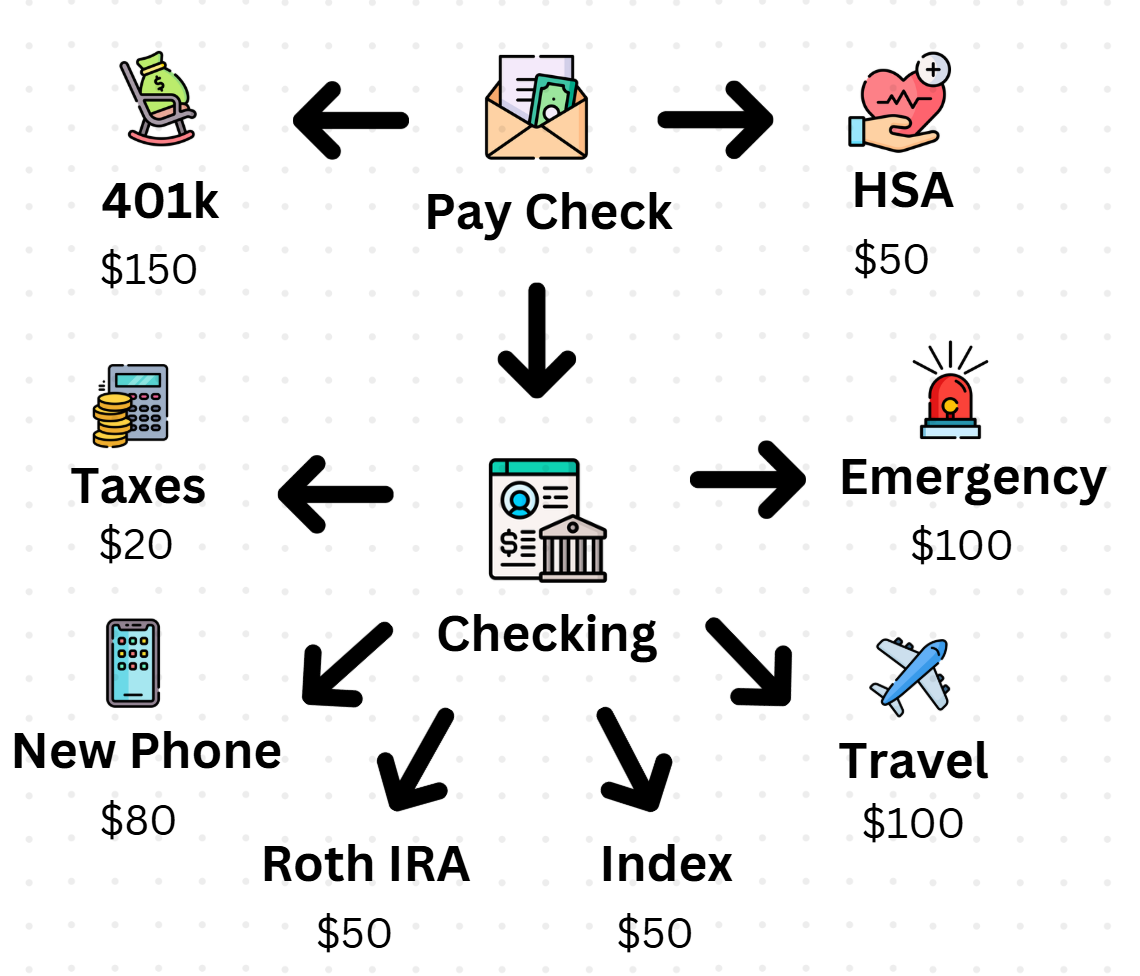

Here’s a simple example if you can save $600/month:

Set aside $300 for the next section (investing), and with the other $300 do this:

- Pick a few things you want to save for in high yield savings accounts (Ex. Emergency, Taxes, Phone, Travel)

- Then distribute that $300 into those accounts

If you plan to spend the money in under 3 years, keep it in savings.

Anything longer than that → invest it (at least that is what the finance gurus say).

💎 Maximizing Investing (Year 7+)

The biggest mistake people make?

Waiting to invest until they “feel rich enough.”

I was investing while $85k in debt.

Using that money we set aside above ($300/month) here’s how I’d split it up:

- $150 → employer 401k

- $50 → HSA

- $50 → Roth IRA

- $50 → brokerage account (low‑cost index funds)

As income increases, you slowly scale all of these together.

🎯 Final Thoughts

This is exactly how I grew my net worth into the $500k range before 30 - while starting in debt.

It took years... (yikes!)

But it was also simple and repeatable.

I break this entire framework down in more detail (with visuals) in my latest YouTube video:

If you want to see the full walkthrough, you can watch it here 👇