I have $303,901 invested in the stock market right now.

Now that might sound insane and unrealistic coming from a 29 year old but I used to be in $85,509 in debt when I was 22. 🤦🏼♀️

I have read 30+ finance books over the last 7 years and I figured out wealth (through employment) really comes down to your knowledge about tax advantaged accounts like HSAs, 401ks, Roth IRAs, etc.

So here is the breakdown of my current portfolio:

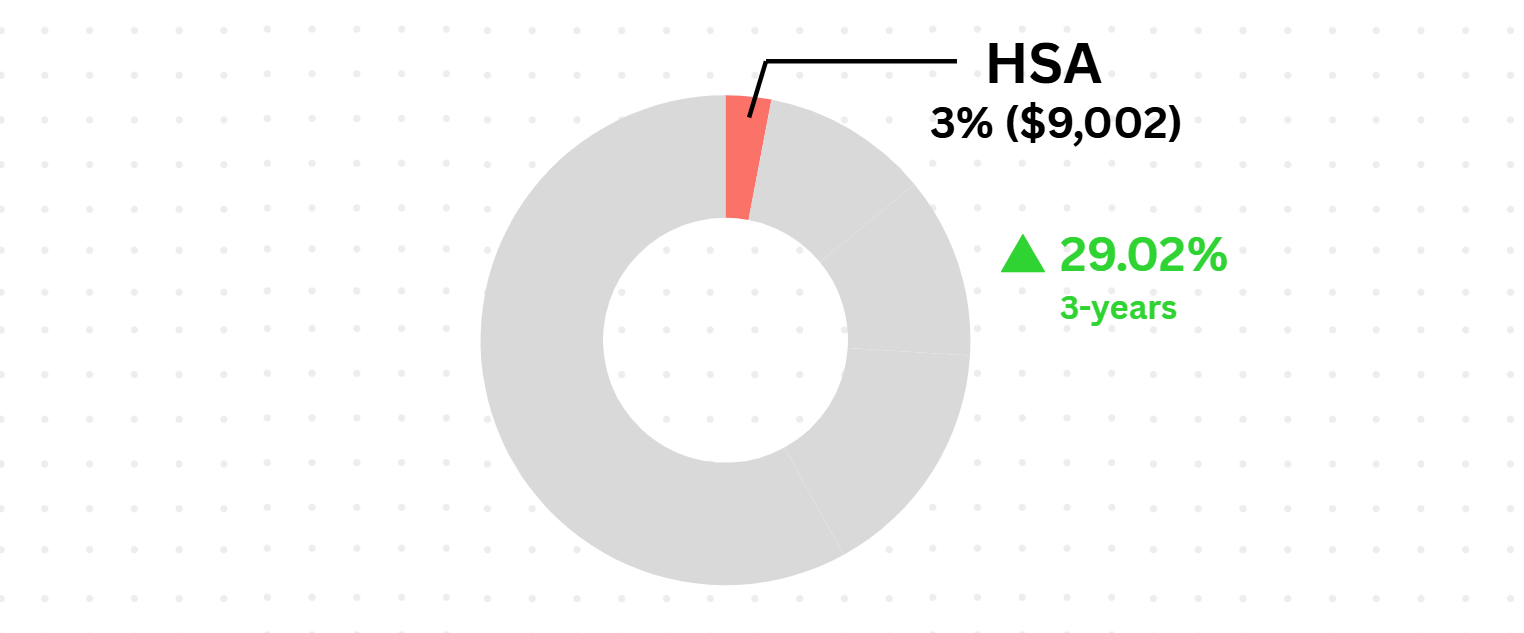

👩🏼⚕️ HSA

Yes, you can invest your HSA in the stock market. It seems odd because its part of your health benefit package as an employee - but it is allowed!

You have to open a high deductible plan to be eligible but it's great because it is triple tax advantaged.

- ⬇️ Reduces Taxable Income - You don't pay income tax on the money you contribute

- 🪴 Tax Free Growth - Investment gains are not taxed while they stay in the account (in most states)

- 🏦 Tax Free Withdrawals - If you use this money for medical expenses you can pull the money out tax free

A lot of people think you can only use this money for medical expenses but that's only if you don't want to pay taxes. If you want to use this money later (65+) for non-medical expenses - all you have to do is pay regular income tax on it.

I pay out of pocket for all my medical expenses and keep the receipts/EOBs set aside. Then I will reimburse myself with the money from my HSA when I am 65. There is no limit on when you can reimburse yourself.

My HSA is in a FFLEX (Fidelity Freedom Index 2060) fund:

- 🎯 Target Date Fund - This means it is targeting a date for retirement and will move my money into more conservative assets like bonds as it gets closer to that date

- 📈 Fund of funds (index) - It buys index funds to match the market

- 🏷️ Expense ratio is 0.08% (this is considered very low which is good)

- 🍰 54% US Stock, 37% Non-US Stock, and 8% Bonds

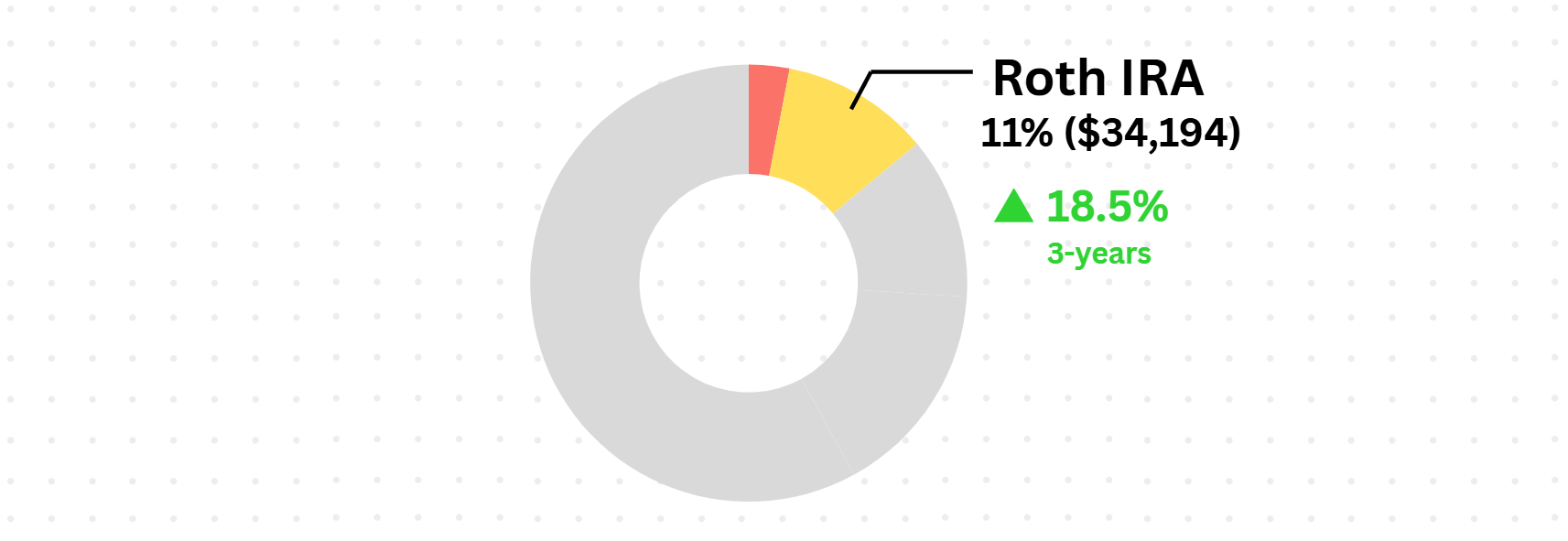

👵🏼 Roth IRA

Now a Roth IRA is already taxed going in, meaning after you get your paycheck and it is deposited into your checking account, you fund this account using that after tax money (the same money you would use to pay rent, pay off credit cards and buy things) - completely outside of your employer.

This means that when you go to pull out your money at 59 1/2 during retirement you don’t have to pay taxes on it.

What I like about Roth IRAs is you can always withdraw the money you contributed without taxes or penalties regardless of age. This is great if you need that money back for emergencies.

However, this is not true for conversions (you have to wait 5 years from when you converted) - which is what you do for a Backdoor Roth IRA. You would use the backdoor method if you make more than $153,000 a year for 2026.

This is how a Backdoor Roth IRA works for reference (max contribution is $7,500 for 2026):

- 🏦 Open and fund ($7,500) a Traditional IRA

- 🔁 Convert the money ($7,500) in your Traditional IRA to a Roth IRA (open one if you don't have one yet)

- 💸 Use the money ($7,500) you funded the Roth IRA to buy a fund within it

In my Roth IRA, I bought a VTTSX (Vanguard Target Date Fund 2060) fund:

- 🎯 Target Date Fund

- 📈 Fund of funds (index)

- 🏷️ Expense ratio is 0.08%

- 💸 Minimum purchase ($1,000)

- 🍰 54% US Stock, 37% Non-US Stock, 8% Bonds

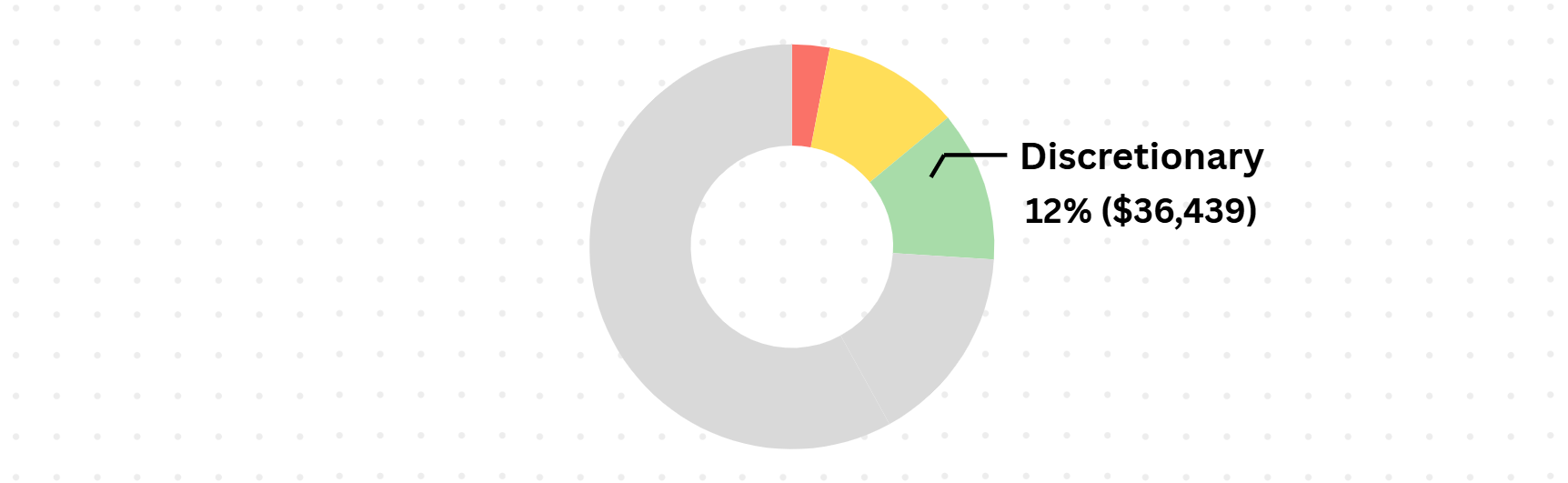

💻 Discretionary Investing

Discretionary investing is outside of your employer typically through a brokerage account website like Wealthfront, Robinhood, etc. I have tried a bunch of different investing strategies over the years:

- 💻 Semiconductor Heavy ($22,433)

- Originally when I was 22, I bought just a ton of semiconductor heavy companies like Lam Research, Micron, AMD, etc. This worked out making 104% ROIs but I think I got lucky.

- ⚓ Anchor ($7,009)

- I have read a ton about how low-cost index funds are the best for balancing diversification, low fees, risk and good returns.

- ⚠️ Risky ($7,034)

- I tried stock picking and I am not sure I can recommend this one, it is a lot of time researching and the payoff so far is minimal. But I will keep you posted!

I am not a financial advisor but my plan is to stick to low cost index funds (otherwise you have to spend your time on quarterly earning calls for the stocks you picked - yuck!).

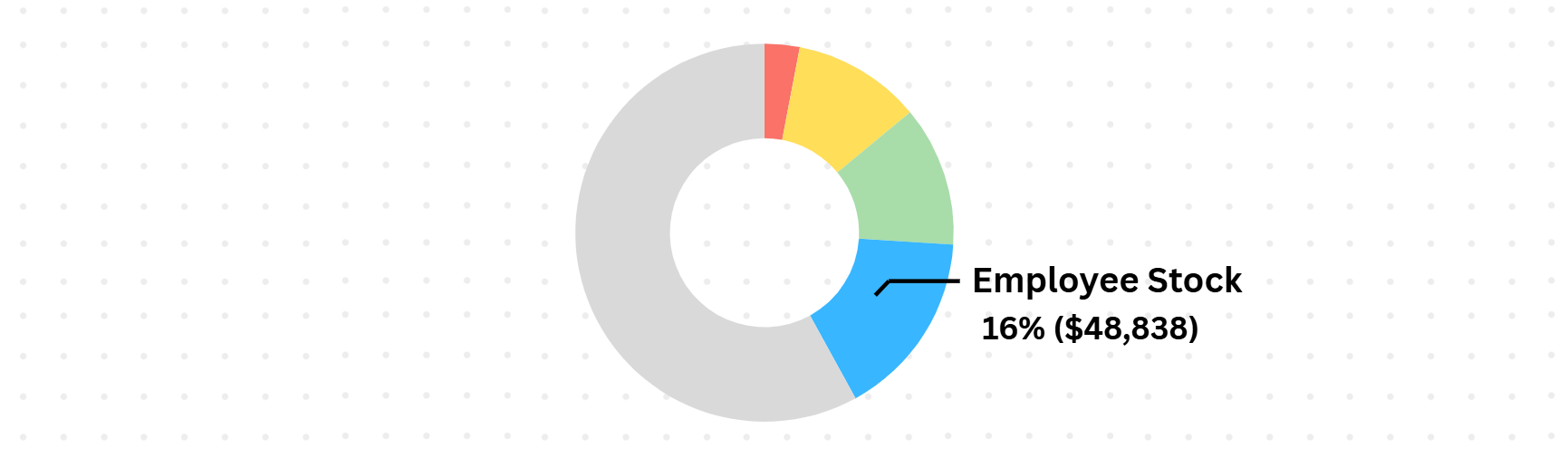

🩵 Employee Stock

Employee stock is not talked about in any of the finance books I read and I think it's a complete miss.

I have found receiving equity through your employer is one of the best ways to grow wealth.

Typically, big companies like Google or Microsoft (and in my case Intel) will give you stock as a signing bonus, yearly bonus or you can buy it at a discount.

Then you can sell it for real cash once you are fully "vested" (which basically means you waited long enough to get the money).

I sold $83,121 of Intel stock recently at it's peak. Then I redistributed it into retirement accounts, index funds, etc - to get it down to 16% of my portfolio. I also set aside $35k of what I sold to freeze my eggs and some other personal investments. It's a complete game changer compared to working for a company without stock options.

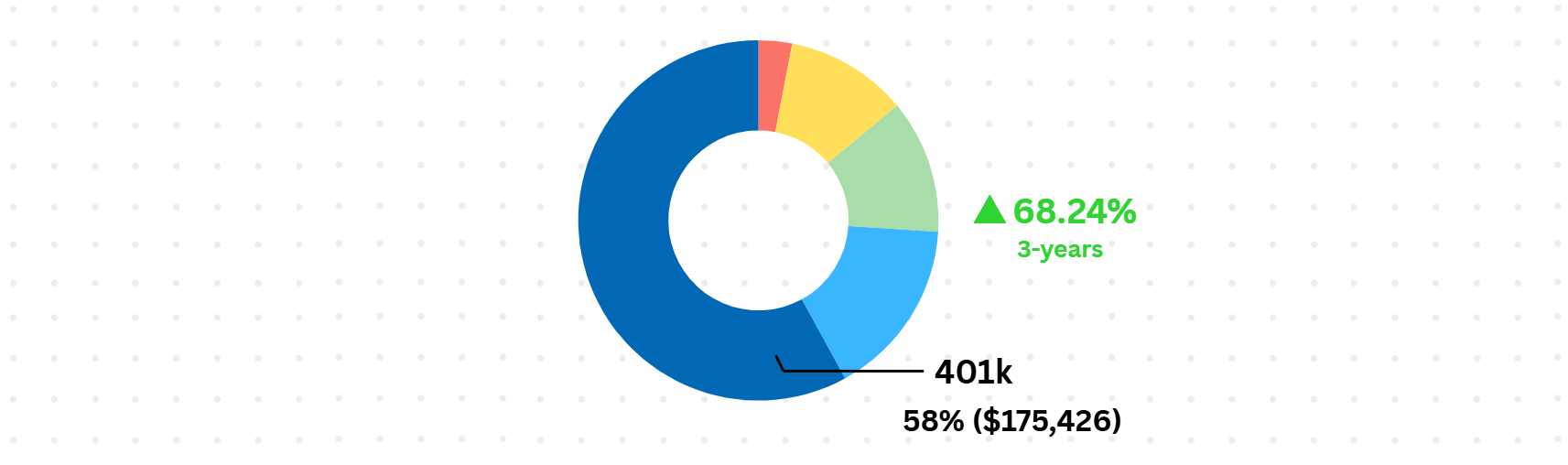

💰 401k

Since I was 22 (even when I was in debt) I always had my 401k contribution at 10-15%. And its crazy to think I barely felt that money being pulled out of my check and all of a sudden I look at my 401k 7 years later and see that balance.

From all the finance books I have read this is always one of the first accounts they mention to open if your employer allows it. Most companies also match a certain contribution (3%-7%) so it's free money!

My 401k is in FDKVX (Fidelity Freedom 2060) which I will be switching to a lower expense ratio fund soon.

- 🎯 Target Date Fund

- 📈 Fund of funds (actively managed)

- 🏷️ Expense ratio is 0.68% - this is considered high and why I want to move my 401k out of this fund

- 🍰 55% US Stock, 40% Non-US Stock, 10% Bonds

🎬 Video

You can watch my full video below 🙌🏼

What makes this video even more special is I get to brag about one of my favorite software applications: Scribe.

Scribe’s AI platform instantly turns workflows into step-by-step guides, SOPs, training manuals, and how-to documentation to help teams get work done.

I use this software to create visual process documentation in seconds (compared to hours of manually screenshotting) - it's perfect for employee onboarding, out of office documentation, internal knowledge bases, and honestly just sharing how work gets done.

I'm so happy to be showcasing a tool that I have used for 3+ years - feel free to try out their free plan here.